Meet two members of the plan.

They did everything right. They contributed consistently, stayed invested, and retired with similar savings. For simplicity, we use the Balanced Fund in this example, though in practice members would typically reduce risk and adjust their asset mix as they approach retirement.

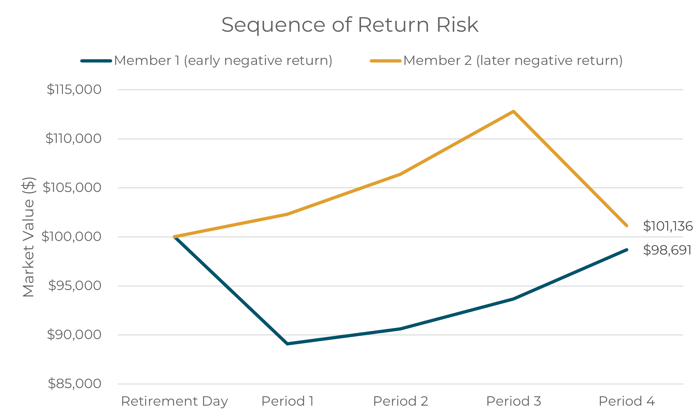

Member 1: Retires December 31, 2021

After years of saving, the first member retires at the end of 2021, confident in their plan. Then reality hits.

-

2022: −5.9%

Early in retirement, they face a meaningful down year.

At the same time, they are drawing income from their portfolio. When markets fall, they can’t simply wait for a recovery. They must sell investments to fund retirement spending, locking in losses.

Here’s what that looks like, starting with $100,000 and withdrawing 5% annually:

| Year | Starting balance | Balanced Fund return | Market Value after return | 5% Withdrawal ($) | Ending balance |

| 2022 | $100,000 | -5.9% | $94,100 | $5,000 | $89,100 |

| 2023 | $89,100 | 7.3% | $95,604 | $5,000 | $90,604 |

| 2024 | $90,604 | 8.9% | $98,668 | $5,000 | $93,668 |

| 2025 | $93,668 | 10.7% | $103,691 | $5,000 | $98,691 |

Despite several good years, the early loss combined with withdrawals make it difficult to build lasting momentum.

Member 2: Retires December 31, 2022

The second member retires one year later.

They avoid the earlier downturn, and their experience begins very differently:

-

2023: +7.3%

-

2024: +8.9%

-

2025: +10.7%

Right from the start, their portfolio is growing even as withdrawals begin.

Here’s the same $100,000 starting point, extended to match the same average return:

| Year | Starting balance | Balanced Fund return | Market Value after return | 5% Withdrawal ($) | Ending balance |

| 2023 | $100,000 | 7.3% | $107,300 | $5,000 | $102,300 |

| 2024 | $102,300 | 8.9% | $111,405 | $5,000 | $106,405 |

| 2025 | $106,405 | 10.7% | $117,790 | $5,000 | $112,790 |

| 2026 hypothetical | $112,709 | -5.9% | $106,136 | $5,000 | $101,136 |

Even after adding a negative year, bringing the average return in line with Member 1, the outcome is still different.

Early gains create a powerful advantage:

-

Withdrawals are a smaller percentage of the portfolio

-

The capital base remains stronger

-

Later losses are easier to absorb

What’s going on here?

This is called sequence of returns risk. It’s not just how much you earn; it’s when you earn it.

-

Losses early in retirement can do lasting damage

-

Gains early in retirement can significantly improve outcomes

Both members experience essentially the same average return. But the order of those returns leads to different results.

Why early retirement years matter most?

The years around retirement, roughly five years before and the first decade after, are the most important. This is when your portfolio is largest, withdrawals begin, and market declines have the greatest impact.

Early declines force you to sell more assets at lower values, reducing the ability to recover later. Strong early returns, on the other hand, provide a cushion that makes future downturns less harmful.

What can you do about it?

Sequence of returns risk can’t be eliminated, but it can be managed. Here’s what you can do to plan for and mitigate sequence of return risk:

-

Know your risk tolerance by considering your age, goals, income needs, and comfort with market fluctuations. Use our Risk Tolerance Calculator to help guide your strategy.

-

Move 2-3 years of anticipated retirement spending to the Money Market Fund, especially if you are planning to use the Variable Benefit product for retirement income to avoid needing to sell equity or fixed income investments during market downturns.

-

Consider the Bond Fund to reduce equity exposure and provide an alternative withdrawal source. Bonds can often go up in value when equity markets are going down.

-

Convert some or all of your CSS retirement savings to CSS’ Fixed Monthly Pension. Get personalized advice from our advisory team to build a retirement plan tailored to your needs and goals.

What comes next?

It is important to ensure your investment mix matches your stage of life. As you approach and enter retirement, balancing growth and stability is crucial.

In our next article, we’ll show how to use the four CSS fund options: Balanced, Equity, Bond, and Money Market, to build and maintain the right mix for your situation, and how rebalancing helps manage risk over time.

If you have questions about this article or want to learn more about sequence of returns risk, please contact us.

.png)